Automation

Mortgage Processing

The Problem: Paper Mountains in a Digital World

Every mortgage loan is a document marathon. A single file can contain 200 or more pages — pay stubs, credit reports, appraisals, tax returns, bank statements, and closing disclosures. For most lenders in 2025, someone is still manually touching every one of them. The numbers tell a punishing story.

$11,800 Avg. cost to originate a loan, Q2 2025 (Freddie Mac)

47 days Average time to close a mortgage (ValuePenguin)

60% Of closing time consumed by document collection & review

Despite years of digitization efforts, 58% of lenders still cite document collection inefficiencies as a top barrier to faster closings (Fannie Mae). Meanwhile, a Fannie Mae Lender Sentiment Survey found that 73% of lenders now rank operational efficiency as their primary driver for adopting AI and ML — up from just 42% in 2018. The pressure is real and accelerating.

The core challenge isn't a lack of technology — most lenders run an LOS, a QC platform, and perhaps a legacy OCR tool. The problem is that none of these systems talk to each other intelligently. Decisions still depend on a human reviewing documents against rules they carry in their heads. Every exception — an inconsistent income figure, a missing signature, a document out of order — requires a manual workflow that adds days to the cycle and cost to the loan.

What the Market Is Building

The Intelligent Document Processing (IDP) market was projected to reach $10.57 billion in 2025, on a trajectory to $66.68 billion by 2032 — a compound annual growth rate of 30.1% (Fortune Business Insights). North America leads with nearly 48% of global IDP market share. Mortgage is one of the largest drivers of that growth.

Several platforms have emerged with varying approaches to solving the document problem in lending:

AI-First Fintech · Underwriting Focus

Automated Document Classification & Income Verification

Classifies and indexes over 1,600 financial document types, pre-populates income calculations, and integrates with major LOS platforms. One mid-sized community bank reduced keystrokes per application from hundreds to fewer than 100 and estimated 8,500 hours in annual staff savings.

Enterprise IDP · Multi-Industry Leader

Mortgage-Tuned Extraction Across the Loan Lifecycle

Covers origination, QC, post-close, and servicing in a single pipeline. Consistently recognized in major analyst evaluations (IDC, Everest Group) for accuracy in document splitting, stacking, and validation at scale.

Global Document AI · NLP-Driven

Structured & Unstructured Content Processing

Goes beyond OCR to extract and interpret both structured data (loan amounts, dates) and unstructured content (contract language). Supports the full mortgage automation lifecycle from point of entry through decisioning, with human roles shifting from manual review to exception oversight.

Banking-Vertical AI · Computer Vision

No-Code QC Workflow & Audit-Ready Analytics

Built for banking and mortgage with multi-layered document identification, no-code compliance workflow management, and real-time dashboards for complete platform activity monitoring and out-of-the-box audit reporting.

Mortgage-Engineered IDP · Private LLMs

End-to-End Origination & Servicing Automation

Covers loan origination through servicing in a single platform using private LLMs for data extraction, cross-validation against predefined rules, and traceable audit trails for compliance and QC transparency.

Common across all these platforms: automation of document classification, data extraction, and rules-based validation. Where they diverge is mortgage-specific depth, LOS integration flexibility, decisioning sophistication, and how they handle the inevitable human exception.

What Good Solutions Actually Do

The evolution in this space is moving through three recognizable stages, and the most capable platforms today are operating across all three simultaneously.

Stage 1 — Documents Become Data

Modern IDP uses LLM-based classification and ML-enabled extraction to convert any document — scanned, handwritten, PDF, electronic — into structured, machine-readable data. A 200-page loan package is split, classified, stacked, and extracted without a human touching it, with accuracy rates approaching 95%.

Stage 2 — Rules Make the Data Useful

Extraction without validation is just fancy OCR. The differentiator is a configurable rules engine that can compare income figures across a 1003, two pay stubs, and a tax return simultaneously — or flag a Closing Disclosure where dates don't align. No-code configuration lets QC and compliance teams update rules without a developer sprint.

Stage 3 — Decisions at Scale with Human Oversight

Automated rules handle clean loans. The real value is in the exceptions. Intelligent decisioning routes flagged files to the right reviewer with full context already surfaced. This human-in-the-loop model means the system handles volume while skilled staff focus on judgment calls — with a full audit trail that holds up to investor or regulatory review.

"Lenders who extensively use digital AI capabilities experience 40% fewer loan defects compared to those with low usage." — Freddie Mac Cost to Originate Study, 2025

The critical infrastructure requirement — one often overlooked in vendor evaluations — is system agnosticism. Lenders have spent years and millions building LOS configurations, and ripping them out to adopt a new platform is not a viable path. The most effective IDP solutions integrate directly into existing LOS workflows, operating as a non-invasive intelligence layer rather than a replacement system.

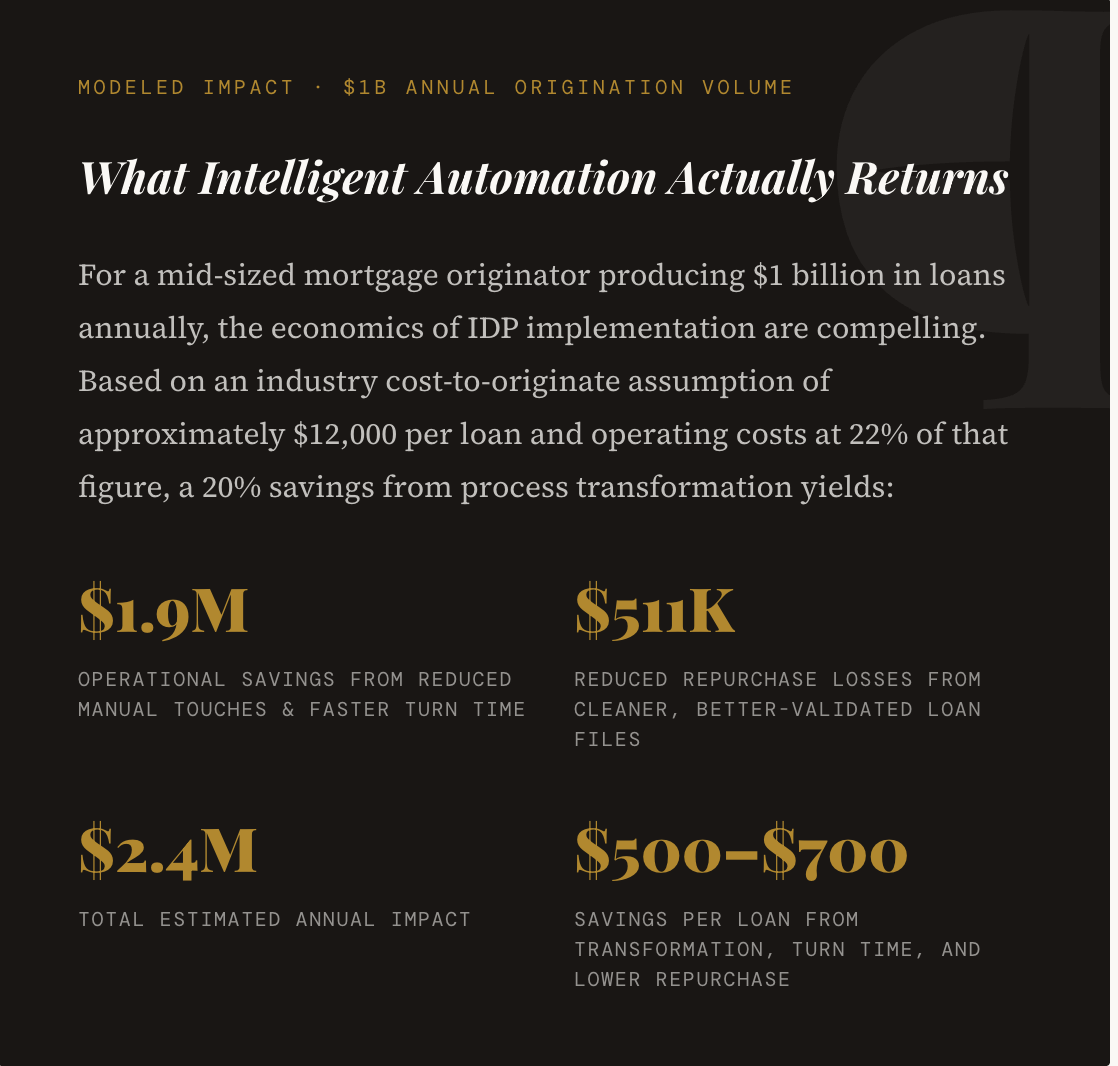

The Financial Case Is Not Subtle

Those per-loan savings matter in a margin-compressed environment. Freddie Mac's 2025 analysis found lenders with extensive digital adoption experience 40% fewer loan defects and up to 50% better Non-Acceptable Quality rates. In a purchase-dominated market, these are not marginal improvements — and the repurchase exposure angle makes it even more concrete. A single repurchase demand can eliminate the margin on multiple loans. IDP-driven QC applied consistently across pre-fund and post-close catches data inconsistencies before they become investor problems.

What Separates a Platform from a Point Solution

As lenders evaluate IDP options, a few criteria separate genuine transformation platforms from glorified OCR tools. Mortgage specificity matters first — generic document AI built for invoices requires extensive rework to handle a 1003, a 4506-C, or a stacked closing package. No-code rules configuration is equally critical: compliance requirements change, and platforms that require developer involvement to update a rule set will always lag the business. Human-in-the-loop architecture ensures that full automation serves the clean files while human judgment is applied to the exceptions that warrant it. And non-invasive LOS integration — system-agnostic deployment that adds intelligence without replacing existing infrastructure — is what makes adoption realistic rather than theoretical.

Alchemist Solutions' Intelligent Digital Platform (IDP) addresses each of these dimensions — combining mortgage-specific AI automation, a no-code configurable rules engine, human-level exception decisioning, and integrated pre-fund and post-close QC — to deliver measurable per-loan cost reduction without disrupting existing LOS workflows. For more information, email info@alchemistsolutions.io